Modern Economic Reality Reveals Shocking Millennial Financial Struggles Despite Record Net Worth Growth

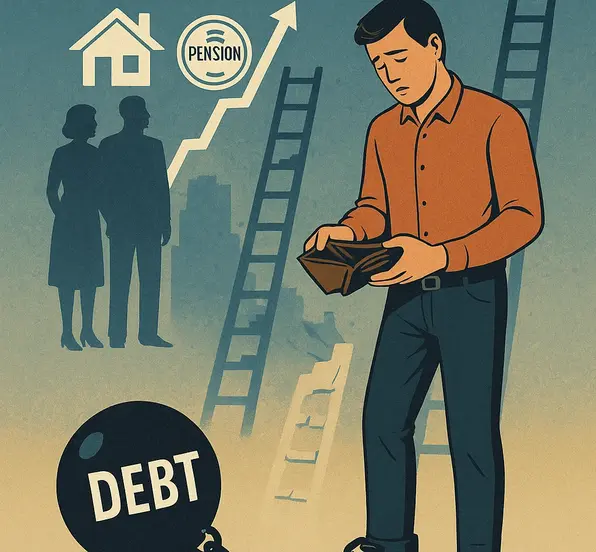

The financial landscape for today’s young adults bears little resemblance to what their parents experienced decades ago. Despite millennial net worth quadrupling from $3.9 trillion to nearly $16 trillion between 2019 and 2024, more than half report living paycheck to paycheck. This paradox of “phantom wealth” highlights the severe millennial financial struggles that define a generation caught between paper prosperity and practical hardship.

When comparing a typical American household budget from 1985 to 2022, most expenses have scaled with inflation—but with critical exceptions. Housing costs, healthcare expenses, and childcare have skyrocketed beyond inflation rates, while retirement costs have increased by more than 60%. Even more concerning is the explosion in consumer debt, which has grown from nearly $600 billion in December 1985 to a staggering $4.9 trillion by 2022.

These millennial financial struggles aren’t the result of frivolous spending on “avocado toast” as some critics suggest. Rather, they stem from fundamental economic shifts that have created two separate economies—one where the American Dream remains accessible, and another where it feels increasingly out of reach despite working full-time jobs.

The Vanishing Middle Class: How Millennial Financial Struggles Are Redefining Economic Classes

The “Big Three” Expenses Crushing Young Adults

The financial challenges facing millennials and Gen Z can be attributed to what experts call the “Big Three” expenses:

• Housing costs that have far outpaced wage growth

• Massive student loan debt payments

• Exorbitant childcare expenses

As Freddie Smith, who transitioned from actor to realtor and content creator, points out: “In the summer of 2023, housing prices hit $420,000, interest rates hit 7%. You now need $120,000 to qualify for a home.” This stark reality has fueled online debates between generations about economic opportunity.

The middle class, as previous generations knew it, appears increasingly out of reach. “I think the middle class, unfortunately, is dead for millennials and Gen Zers,” notes one expert. “Or best case scenario, the goalpost is just moved and it’s still obtainable. But you have to make over six figures to have that middle class life.”

The Homeownership Crisis and Its Long-Term Implications

The inability to purchase homes has created a cascade of financial consequences for younger generations. In the 1980s, the typical first-time homebuyer was in their late 20s with a 30-year mortgage, meaning they could own their home outright by retirement age. This provided financial stability during fixed-income retirement years.

Fast forward to 2024, and the median first-time homebuyer is now 38 years old—an all-time high. This delayed entry into homeownership has profound implications for retirement planning and overall financial security.

“Those who don’t own homes now, those are people who are in real trouble,” explains one financial expert. “They’re trying to save to get their own place. They’re paying high rent somewhere. They’re commuting a long distance or trying to work at home so they can save on childcare, or so they can save just on housing costs.”

The national housing shortage, combined with high rent prices and competition from wealthier buyers, has created a perfect storm for millennial financial struggles in the housing market.

Income Volatility: The Hidden Factor in Millennial Financial Struggles

When Traditional Financial Advice Falls Short

Many Americans are navigating a new kind of economic instability that traditional financial advice simply doesn’t address. Rachel Schneider, co-author of “The Financial Diaries,” spent a year tracking the detailed spending habits of 235 families and discovered something surprising.

“What we saw was a huge amount of volatility. That was our core finding,” Schneider explains. “The majority of Americans work hourly jobs. And so for them, the amount of money that they earn fluctuates week by week. I get 30 hours this week versus 45 hours next week. And so as a result, income is really up and down over the course of a month. And that flies in the face of all of the budgeting advice we usually give people.”

This income instability creates a fundamental disconnect between financial advice and financial reality for many millennials. Traditional budgeting assumes consistent income, but the gig economy and hourly work have made income unpredictability the norm for many young adults.

The Difference Between Surviving and Thriving

The current economic landscape has created a situation where many young adults are merely surviving rather than thriving, despite working full-time jobs.

“There’s a difference between surviving and thriving,” notes one economist. “And I just think if we’re going to claim that we’re the richest country, the best country in the world, why isn’t everyone who’s working 40 hours, 50 hours a week thriving? How is that possible?”

This question cuts to the heart of millennial financial struggles. Despite following traditional paths to success—education, hard work, fiscal responsibility—many find themselves unable to achieve the financial milestones their parents reached at similar ages.

“If someone got straight A’s in school, straight A’s in college, got a bachelor’s, got a master’s degree and is 29, making $80,000 and can’t even get their own apartment, let alone purchase a house or have financial stability… that’s where I think there’s something broken in the system.”

The Myth of Overspending: Debunking Misconceptions About Millennial Financial Struggles

Beyond Avocado Toast: The Real Causes of Financial Insecurity

A common narrative suggests that millennial financial struggles stem from poor spending habits—the infamous “avocado toast” argument. However, the data tells a different story.

“What the historians tell us is that every single new generation gets complaints from the older generation about how they’re behaving irresponsibly, immorally,” explains one financial historian. The reality is that structural economic factors, not spending habits, are the primary drivers of financial instability for younger generations.

While it’s true that some individuals may overspend, the broader trend shows that even financially conscious millennials with good incomes and education are struggling to achieve basic financial milestones.

“I think that’s why there’s so much confusion,” notes Smith, “because you can point to a millennial who spends $1,200 on DoorDash. Not good. But you can also point to a millennial who’s very financially conscious, making 80,000 and is drowning in debt and is living with a roommate and is a lawyer at 29 years old. That is not right.”

The Shifting Burden of Financial Security

Even as household wealth has increased on paper, Americans now bear more individual responsibility for financial security than previous generations did.

“Americans are now largely on their own when it comes to things like insurance, retirement savings, healthcare,” explains one economist. “That makes it harder just across the board to feel financially secure.”

This individualization of financial risk has created a situation where even as prices have risen significantly, consumer spending patterns haven’t changed much. The result? More Americans relying on credit cards to make ends meet at the end of the month, further exacerbating millennial financial struggles.

Finding Solutions: Practical Approaches to Millennial Financial Struggles

Individual Strategies for Financial Stability

While systemic changes are needed to address the root causes of millennial financial struggles, individuals still need practical strategies to navigate the current economic landscape. Financial experts offer several approaches:

• Create a savings habit, even if it’s small at first

• When receiving a promotion or raise, maintain your current lifestyle temporarily to build savings

• Take advantage of online classes, certification programs, and other upskilling opportunities

• Consider creative housing arrangements like co-living with friends

• Explore shared childcare arrangements across families

“I always encourage people, once you do get that promotion, just stay where you’re at for a while and just accumulate money, even for just a year,” advises one financial planner. “Maybe buy yourself something nice, but just keep that money for a little while and just enjoy the freedom, because all of a sudden you’re not as fearful at work because you got a little cushion.”

Embracing Community Solutions

As individual financial independence becomes more challenging, community-based approaches may offer both practical benefits and emotional support.

“We’re going to see people cohabitating with friends for longer and coming up with creative ways to share childcare across families, because that’s what it’s going to take to make it work,” predicts Schneider. “And actually, we’re going to see, I think, some real benefits in community that could come out of that.”

This perspective offers a potential silver lining to millennial financial struggles: “I might not be able to be as independently financially stable, but what does that mean for the interconnections I can and should create with other people?”

Looking for Financial Career Opportunities?

The financial landscape may be challenging, but there are still paths to success in today’s economy. From financial planning to fintech careers, opportunities exist for those with the right skills and knowledge.

Explore finance job opportunities on WhatJobs and position yourself for success in today’s evolving economic environment.

Search Finance Jobs →FAQ

What are the main causes of millennial financial struggles in today’s economy?

Millennial financial struggles stem primarily from three major factors: skyrocketing housing costs that have far outpaced wage growth, massive student loan debt burdens that previous generations didn’t face, and extremely high childcare expenses. Unlike their parents, millennials are dealing with these “Big Three” expenses simultaneously while also experiencing more income volatility from gig work and hourly positions. Additionally, the responsibility for retirement savings, healthcare costs, and other financial security measures has shifted from employers to individuals, creating further financial pressure.

How have millennial financial struggles impacted homeownership rates among young adults?

Millennial financial struggles have dramatically altered homeownership patterns. In the 1980s, the typical first-time homebuyer was in their late 20s, but in 2024, the median age has risen to 38—an all-time high. This delay has serious implications for long-term financial security, as previous generations could own their homes outright by retirement age, providing stability during fixed-income years. Today’s housing market, characterized by limited inventory, high prices, and elevated interest rates, requires an income of approximately $120,000 to qualify for an average home, putting homeownership out of reach for many millennials despite their education and career advancement.

Are millennial financial struggles really caused by poor spending habits as some suggest?

Despite popular narratives about “avocado toast” and frivolous spending, research shows that millennial financial struggles are primarily structural rather than behavioral. While individual spending choices matter, even financially conscious millennials with good incomes and education often struggle to achieve basic financial milestones their parents reached at similar ages. The data reveals that housing costs, healthcare expenses, and childcare have all increased far beyond inflation rates, while consumer debt has grown from $600 billion in 1985 to $4.9 trillion by 2022. These systemic economic shifts, rather than spending habits, are the primary drivers of financial instability for younger generations.

What practical solutions exist to address millennial financial struggles in today’s economy?

Addressing millennial financial struggles requires both individual strategies and systemic changes. On a personal level, financial experts recommend creating consistent savings habits regardless of amount, maintaining your current lifestyle temporarily after receiving raises to build financial cushions, and pursuing upskilling opportunities through online classes and certification programs. Community-based approaches are also emerging as viable solutions, including co-living arrangements with friends and shared childcare across families. These collaborative approaches not only provide financial benefits but can also create valuable social connections. Additionally, policy changes addressing housing affordability, student debt relief, and childcare costs would help alleviate the structural barriers facing millennials.