Economists are sounding alarms that the U.S. economy may already be in a recession, with several key labor market indicators flashing red and drawing comparisons to the early 2000s dot-com crash and the 2007 financial crisis. The warnings come amid growing controversy over federal employment statistics and heightened concerns about a fragile housing market still struggling with affordability pressures.

Weak Job Growth Raises Alarms

The Bureau of Labor Statistics (BLS) reported that U.S. job growth slowed sharply to just 77,000 in July 2025, well below expectations. Even more concerning, earlier months saw significant downward revisions. On a year-over-year basis, employment growth is now below 1%, a threshold that historically has coincided with recessions.

“This level of job growth is almost identical to what we saw in late 2007, just before the Great Recession, and in early 2001, right before the dot-com bust,” one labor economist explained. “It’s not speculative to say the labor market has turned for the worse. The data is consistent across multiple measures.”

Political Controversy at the BLS

The weak report was quickly engulfed in political drama. Former President Donald Trump accused the BLS leadership of being partisan and alleged that job numbers were being “rigged.” In a controversial move, Trump dismissed the head of the BLS, raising questions about the independence and credibility of future labor market reporting.

The shake-up has divided analysts and investors. Some argue the numbers reflect an undeniable slowdown, while others fear that politicizing the data could damage confidence in official statistics at a critical moment for the economy.

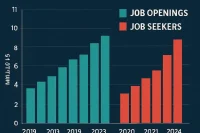

Alternative Labor Market Measures Point to Recession

Beyond the BLS figures, several independent indicators confirm the downturn:

- Indeed Job Openings Index: Job postings have fallen to 105, down 35% from pandemic peaks and now near pre-pandemic levels.

- ISM Manufacturing Employment Index: Employment in manufacturing is contracting at the fastest pace in a decade, excluding the pandemic.

- ISM Services Employment Index: Dropped to 46.4, its third-lowest reading in 10 years, signaling employers in the services sector are also cutting jobs.

“These are not isolated signals,” said one analyst. “When you see broad-based weakness across manufacturing, services, and job postings, it’s clear the slowdown is real.”

Public Perception: Americans Already Feel Recession

Polls show the public largely agrees with economists’ warnings. A recent survey found that 68% of Americans believe the U.S. is already in recession, with more than 80% saying they either believe a downturn has begun or is imminent.

Three years of inflation, stagnant wage growth, and unaffordable housing have eroded consumer confidence. White-collar workers—particularly recent graduates in finance, tech, and engineering—are reporting heightened difficulty finding jobs, echoing early signs of previous recessionary cycles.

Support Workers in a Challenging Economy

Post your job on WhatJobs and connect with qualified professionals—help recent graduates and experienced talent find opportunities during uncertain times.

Post a Job Now →Housing Market: Still in a Bubble?

The slowdown is especially concerning for the housing sector, which remains burdened by high prices and limited affordability. Despite higher mortgage rates cooling demand, prices have remained stubbornly elevated.

The average monthly mortgage payment across the U.S. is now $2,800, a level far above affordability benchmarks. Analysts estimate that for housing demand to recover, two conditions may be necessary:

- A 20% decline in home prices

- Mortgage rates dropping to around 5%

Under that scenario, average monthly payments would fall closer to $1,950, making homeownership viable again for many Americans.

But current forecasts suggest only a modest 1–2% decline in prices over the next year. More significant corrections would likely require a deeper recession and broader job losses, which could trigger distress sales and increased supply.

Fed Policy: Behind the Curve?

Critics say the Federal Reserve is already late in cutting rates to support the weakening labor market. Comparisons with past downturns are stark:

- In 2001, the Fed began cutting rates when job growth was still at 1.4% year-over-year, stronger than today’s 0.97%.

- In 2007, the Fed cut rates at similar employment growth levels, months before the financial collapse fully unfolded.

In both cases, the Fed acted sooner than it has in 2025. Analysts warn that waiting longer could make the recession deeper and more painful.

Homeowner Equity at Record Highs — and Unsustainable

One striking factor is the level of homeowner equity. U.S. households collectively hold about $34 trillion in home equity, nearly three times the level seen in 2006. Equity now exceeds 115% of GDP, the highest ratio on record.

“This is phantom wealth,” said one housing market strategist. “It looks good on paper, but it’s not supported by fundamentals like wages or rental income. A correction of 15–20% in home prices wouldn’t erase homeowners’ financial stability—it would simply bring valuations back in line with reality.”

Market Outlook and Buyer Strategies

While some fear a housing crash akin to 2008, analysts argue the risks are different this time. In 2008, a 25% decline left millions underwater on their mortgages. Today, homeowners generally have far more equity, giving them room to absorb a correction without triggering widespread defaults.

For buyers, the downturn may present opportunities. Real estate analytics platforms, such as Reventure App, are advising clients to use price forecasts in negotiations. Early adopters report saving $50,000 to $80,000 on purchases by leveraging market data to push sellers toward realistic pricing.

What Comes Next?

The coming months will be critical. If the Fed cuts rates in September but housing prices remain inflated, analysts say demand is unlikely to recover quickly. True affordability may only return once sellers begin accepting lower valuations.

The broader economy, meanwhile, faces the risk of job losses accelerating, further dampening consumer confidence and spending. With historical comparisons to 2001 and 2007 piling up, many believe the U.S. is already at the start of its next recessionary cycle.

FAQs

1. Are we already in a recession?

Many economists believe the U.S. is effectively in a “job market recession.” Job growth is below 1%, and multiple indicators—including ISM surveys and job postings—point to contraction. Official declarations may lag, but the data is consistent with past pre-recession periods.

2. Will housing prices fall significantly in 2025?

Baseline forecasts suggest a modest 1–2% decline. However, if job losses mount and a full recession unfolds, a 15–20% correction is possible, especially in overheated metro markets.

3. Why hasn’t the Fed cut rates yet?

The Fed has prioritized fighting inflation, which remains above target. However, critics argue the central bank is “behind the curve” compared with 2001 and 2007, when rate cuts came earlier in response to weaker labor markets.

4. Should homebuyers wait or buy now?

For many, patience may pay off. If prices decline even modestly and rates ease, affordability will improve. But buyers willing to negotiate aggressively using data may already find opportunities to secure below-market deals in 2025.