Are we in an AI bubble — the $800 billion warning signs

Are we in an AI bubble? While Nvidia just hit a $4.5 trillion market cap and AI stocks are pushing the S&P 500 to dot-com bubble levels, there’s an $800 billion debt bomb ticking in the shadows that almost nobody is talking about. When it explodes, it could take your entire portfolio with it. The companies that are supposed to fund the entire AI infrastructure boom are quietly imploding, and the math behind what’s happening is absolutely stunning. If you own tech stocks, index funds, or anything tied to the AI boom, you need to understand the circular financing scheme that Wall Street is using to prop up valuations because history shows us exactly what happens when vendor financing circles collapse.

The circular financing scheme exposed

How the infinite money glitch works

To understand are we in an AI bubble, you need to see the circular financing scheme that’s propping up the entire AI infrastructure boom. Here’s how it works: OpenAI needs computing power to train its AI models, so they go to Oracle and sign a massive $300 billion deal over 5 years. Oracle stock jumped 43% when they announced it, but here’s the problem—Oracle doesn’t actually have $300 billion sitting around. They have a debt-to-equity ratio of 500%, meaning they have five times more debt than equity.

The vendor financing circle

So what does Oracle do? They go to Nvidia and say they need $300 billion worth of chips and infrastructure. Nvidia sells them the equipment, then turns around and invests or provides vendor financing back to OpenAI and other AI companies. It’s money going around in a circle: OpenAI sends money to Oracle, Oracle sends money to Nvidia, Nvidia sends the money back to OpenAI. JP Morgan calls it the “infinite money glitch,” while Goldman Sachs’ head of Delta 1 Trading calls it an “increasingly grotesque vendor financing circle.”

Why this is different and dangerous

Vendor financing isn’t inherently bad—Apple does this with upgrade programs, and car companies do it all the time. But what makes this different and dangerous is that these companies don’t have the cash from operations. Oracle’s cloud infrastructure revenue is projected to go from $18 billion to $144 billion in 2030, requiring everything to go perfectly right for four straight years with no recession, no competition, and no problems. They’re funding it with massive new debt, potentially needing to borrow $25 billion per year—$100 billion over the next four years just to build data centers for this one OpenAI deal.

The $800 billion funding gap

The staggering math behind AI infrastructure

According to Morgan Stanley, the total global data center spend through 2028 will be about $2.9 trillion, broken down as $1.6 trillion on hardware (chips and servers) and $1.3 trillion on building the infrastructure around it. This represents an investment need of over $900 billion every single year. To put this in perspective, the entire S&P 500—all 500 companies combined—spend about $900 billion in all of their investments on everything, not just AI. So we’re basically saying AI infrastructure alone will require the entire capital spend in one year as every major corporation in America spends on everything combined.

Where the money is supposed to come from

Let’s break down the funding sources: Big tech companies like Meta, Apple, Amazon, and Microsoft can self-fund about $1.4 trillion from their cash flow over the next four years. Debt issuance could provide about $200 billion in regular bonds. The securitized market could provide another $150 billion in asset-backed securities and commercial mortgages tied to data centers. Private equity, venture capital funds, and sovereign money could provide $350 billion. But even after adding up all these sources, we’re still $800 billion short—some estimates say as much as $1.5 trillion is missing.

The private credit collapse

Private credit was supposed to be the hero that fills this gap. Firms like Blackstone, Blue Owl, Apollo, and Ares raise money from pension funds, insurance companies, and wealthy individuals, then lend it out at higher interest rates to companies that can’t access traditional financing. But here’s the problem nobody’s talking about: while Nvidia hits record market caps and AI stocks continue to soar, private credit firms are collapsing. Blackstone’s secured lending fund (BXSL) is tanking, massively underperforming the S&P and hitting its lowest levels in over two years. Blue Owl Capital (OWL) is falling off a cliff while tech stocks soar.

Why private credit is imploding

Consumer credit exposure crisis

Private credit firms aren’t just lending for AI infrastructure—they’re heavily exposed to consumer credit, including buy-now-pay-later, auto loans, and personal loans. Non-performing loans are skyrocketing because the low-income crowd got crushed by inflation and now they’re starting to repay student loans again. This creates a perfect storm of financial stress that’s hitting private credit firms hard.

The $5 trillion private equity problem

According to the Financial Review, private equity is sitting on $5 trillion of “existential dread.” A staggering 18,000 private capital funds are trying to raise trillions of dollars simultaneously, which is usually a sign something is about to break. The problem is that they promised very high interest rates and high returns from high-interest loans, but these aren’t materializing as expected because default rates are rising, refinancing is becoming difficult with higher interest rates, and the whole model is under stress.

The canary in the coal mine

These private credit firms are the companies that are supposed to provide that extra $800 billion in funding, and the market is telling you they’re in serious trouble. When the companies that are supposed to fund the AI boom are collapsing while AI stocks soar, that’s your canary in the coal mine—a clear warning sign that the foundation of the AI infrastructure boom is crumbling.

When Finance Falters, Talent Still Wins

As private credit firms stumble and markets grow uncertain, one truth remains: skilled talent is the strongest investment any company can make. Post your job on WhatJobs today and connect with professionals ready to drive resilience and growth.

Post a Job Free for 30 Days →What happens when the funding gap can’t be filled

Option A: AI spending gets cut dramatically

If private credit can’t fill that $800 billion gap, one of three things has to happen. Option A: AI spending gets cut dramatically. Companies slash their projections, data centers don’t get built, and the entire AI infrastructure boom slows down. What happens to Nvidia’s $4 trillion market cap if spending drops 30-40%? The math is devastating for tech stock valuations.

Option B: Hyperscalers take on massive debt

Option B: Hyperscalers like Microsoft and Amazon take on massive debt themselves, leveraging up their balance sheets like Oracle did. This would be unprecedented and risky because remember, Oracle has a 500% debt-to-equity ratio. If hyperscalers go down that route, what happens when the next recession hits? This creates massive leverage risk for the Magnificent Seven.

Option C: Government steps in with massive subsidies

Option C: The government steps in with massive subsidies and guarantees to keep the AI boom going. This could work but creates a huge moral hazard for taxpayers and systematic risk. None of these options are particularly bullish for your portfolio in the traditional sense—Option A crashes tech stocks, Option B creates massive leverage risk, and Option C might keep things inflated longer but creates huge systematic risk.

The dot-com parallel: history repeating itself

Stage 1: New technology emerges with revolutionary potential

We’ve seen this movie before. Go back to 1998: the internet was revolutionizing everything. Companies like Global Crossing were building massive fiber optic networks across the world. The stock soared, everyone knew the internet was the future, and they were right—the internet was the future. But Global Crossing still went bankrupt in 2002. Why? Because they built too much, too fast, funded with too much debt before the revenue could possibly catch up.

Stage 2: Money floods in, returns look good, spending accelerates

The capital circle always turns in these infrastructure buildouts. Stage 1: New technology emerges with revolutionary potential, early investors make huge returns (that was 2022-2023 for AI). Stage 2: Money floods in, returns look so good everybody pours in and spending accelerates, valuations soar (that’s right now). Stage 3: Competition intensifies, more players enter, everybody’s building the same thing and you get overcapacity (we’re getting there—remember DeepSeek).

Stage 4: Promised returns collapse, prices fall, debt comes due

Stage 4: The promised returns collapse because we have too much supply, not enough demand. Prices fall, debt comes due, and the weakest players fail. Stage 5: Consolidation—only the strongest survive, debt gets restructured or written off, investors take massive losses, and eventually the technology succeeds, but most investors lose money.

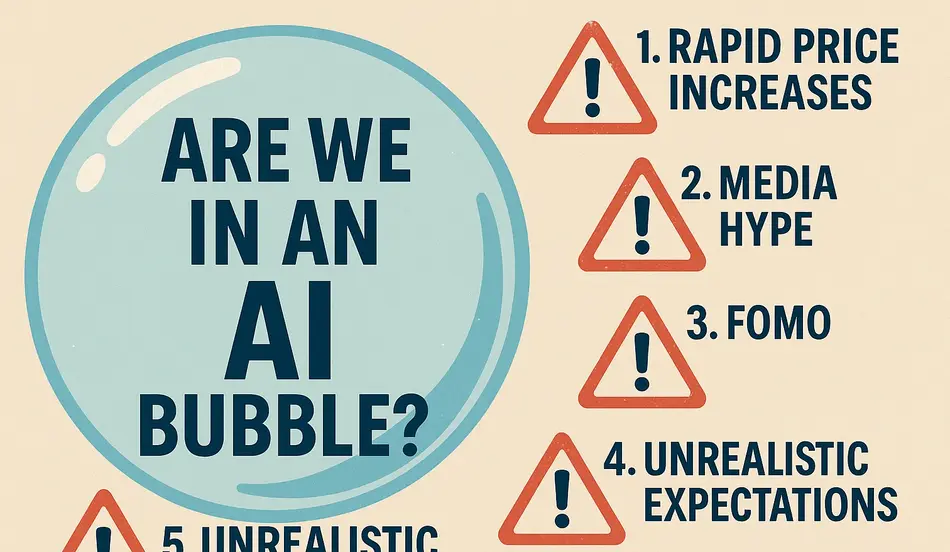

The bubble warning signs

Valuations hitting dot-com levels

The dot-com parallel is striking. Then: “The internet changes everything,” valuations hit record highs, companies spend billions on infrastructure, vendor financing props up the entire ecosystem, and everybody says “it’s different this time.” Now: “AI changes everything,” S&P valuations are near dot-com levels, companies are planning to spend almost $3 trillion on infrastructure, vendor financing is propping up the ecosystem, and everybody is saying “it’s different this time.”

Bubble concerns peaking before the crash

According to Deutsche Bank, web searches for “AI bubble” peaked in August this year and then plummeted. You know what happened around the dot-com bubble? Concerns peaked in late 1998, well before the actual crash in 2000. Bloomberg put out a story in late 1998 quoting an investment manager saying “this is a serious bubble.” NASDAQ was at 2000—it went to 5000 16 months later and then collapsed. When everybody stops talking about the bubble, that’s often when you’re closest to the top. Right now, concerns about the AI bubble have dropped to just 15% of the August concerns.

The infrastructure was real, but the financing wasn’t

The infrastructure was real, the technology was real, the potential was real, but the financing—they couldn’t afford it. This is exactly what’s happening with AI infrastructure today. The technology is revolutionary, the potential is enormous, but the financing model is fundamentally flawed and unsustainable.

How to protect your portfolio

Learn when to sell like the smart money

I’m not saying run out and sell all your tech stocks because we could potentially go a lot higher. What I’m saying is make sure your gains don’t become losses. If you let that happen, then this entire rally that’s hopefully been making you wealthier will be given away. Learn when to sell the way the smart money sells—it’s much simpler than you think, but it’s also not what you think.

Stay informed about AI news and market movements

Stay abreast of AI news and market movements. Create a watchlist with all the AI stocks and turn on notifications for news that actually moves the market. Don’t get distracted by noise, general chatter, or irrelevant information that doesn’t affect your stock prices. Focus only on the news that matters for your investments.

Prepare for the inevitable correction

History shows us that these infrastructure buildouts always follow the same pattern. The technology succeeds, but most investors lose money because they don’t know when to sell. The key is understanding the warning signs and having a plan for when the bubble inevitably pops.

FAQs

Q: What are the main warning signs that are we in an AI bubble?

A: The main warning signs include the $800 billion funding gap, circular vendor financing schemes, private credit firms collapsing, valuations hitting dot-com levels, and bubble concerns dropping to just 15% of peak levels.

Q: How does the circular financing scheme work in are we in an AI bubble?

A: The circular financing scheme involves OpenAI paying Oracle, Oracle paying Nvidia, and Nvidia providing vendor financing back to OpenAI, creating an unsustainable money loop that props up valuations without real cash flow.

Q: Why are private credit firms collapsing in are we in an AI bubble?

A: Private credit firms are collapsing due to consumer credit exposure, rising default rates, the $5 trillion private equity problem, and their inability to provide the $800 billion needed to fund AI infrastructure.

Q: What should investors do if are we in an AI bubble is true?

A: Investors should learn when to sell like smart money, stay informed about relevant AI news, prepare for inevitable corrections, and ensure their gains don’t become losses when the bubble pops.

Live example — user point of view

I was heavily invested in AI stocks when I first heard about are we in an AI bubble concerns. My portfolio was up 40% on Nvidia, Microsoft, and other AI-related stocks, and I was feeling confident about the future. But after learning about the $800 billion funding gap and seeing Blackstone’s private credit fund collapse while AI stocks soared, I realized I was in a dangerous position. I started taking profits systematically, selling 25% of my AI positions when they hit new highs. When the circular financing scheme was exposed, I reduced my exposure further. Now I’m positioned defensively with stop-losses in place and a clear exit strategy. The technology is real and will succeed, but I’m not willing to lose my gains when the financing bubble inevitably pops. My advice: don’t be the last one holding the bag when the music stops.