The way Americans pay for everyday purchases is changing fast — and the shift could challenge the decades-long dominance of credit cards. The buy now, pay later (BNPL) market, led in the U.S. by Klarna, Afterpay, and Affirm, has exploded in popularity since 2019, offering shoppers interest-free installment loans at checkout for everything from $500 jackets to $41 burrito bowls.

BNPL transactions in the U.S. have multiplied 20-fold since 2019, with adoption spreading from online retail to groceries, travel, and even in-store purchases. But as the industry grows, so do concerns over consumer debt, credit risk, and regulatory oversight.

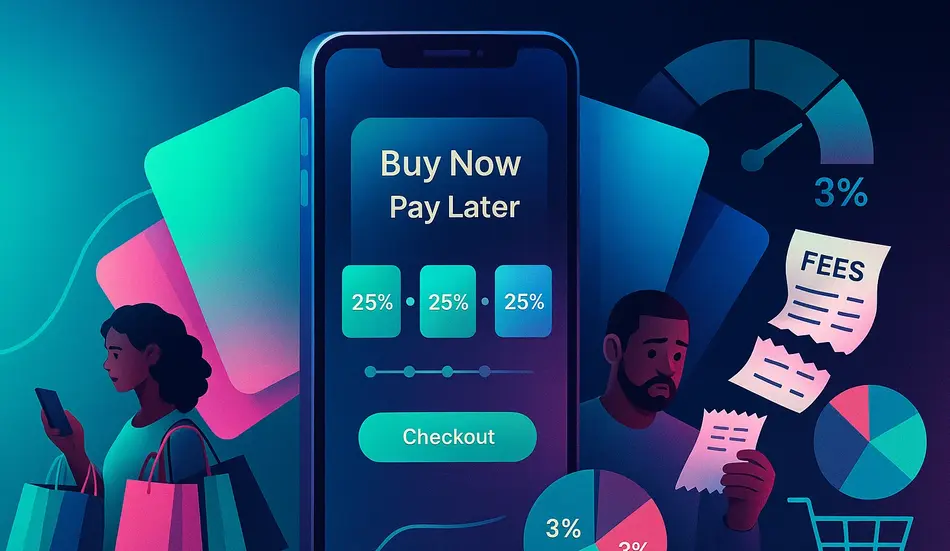

How BNPL Works — and Why Merchants Love It

The core BNPL model is straightforward:

- Customers choose the BNPL option at checkout (often “pay in four” installments).

- The BNPL provider instantly approves the loan based on its underwriting model.

- The merchant receives full payment within a day.

- The BNPL provider assumes the nonpayment risk and collects repayments over time.

Merchants pay for the service — often up to 5% of the transaction value — because BNPL boosts conversion rates and order sizes. For BNPL companies, over 90% of revenue comes from merchants, not consumers.

Some BNPL players, such as Affirm, also offer longer-term installment loans with interest for big-ticket purchases. Afterpay has rolled out a monthly payment option with simple interest for higher-value transactions where pay-in-four is less suitable.

The Push Into Physical Retail

BNPL is no longer just for online shopping carts. Providers are issuing physical payment cards linked to BNPL accounts that can be used in brick-and-mortar stores. This could double the industry’s potential market.

Example: A shopper gets pre-approved for a $500 jacket loan via a BNPL app. The loan sits in the account until they pay with the BNPL card in-store, at which point the transaction is finalized, and repayment begins.

Fintech Is Changing Payments—Is Your Hiring Keeping Up?

As BNPL leaders like Klarna, Afterpay, and Affirm reshape consumer credit, WhatJobs helps you secure talent with the skills to thrive in the new financial landscape.

Post a Job Now →Walmart’s Exclusive Klarna Deal and the Battle for Merchants

Direct merchant partnerships are a critical battleground. In March 2025, Klarna signed an exclusive deal with Walmart to offer BNPL loans through the retailer’s fintech arm, OnePay. These arrangements lock in transaction volumes and make it harder for competitors to capture market share.

Analysts say the BNPL sector still has “white space” — untapped categories and transactions — making expansion more important than fighting over existing retail clients.

From Electronics to Groceries: BNPL’s Expanding Reach

BNPL began in e-commerce with average ticket sizes of $100–$200. Now, it’s used for smaller purchases, including consumables. A LendingTree survey found that 25% of BNPL customers have used it to buy groceries, up from 14% in 2024.

This shift raises questions about whether more consumers are using BNPL for necessities due to financial strain — or simply as a budgeting tool.

“We don’t judge how customers choose to pay,” Affirm said. “Any time a consumer chooses Affirm over a credit card, that’s a win.”

The Credit Risk Question

The Consumer Financial Protection Bureau (CFPB) reported in January 2025 that over two-thirds of BNPL loans went to borrowers with lower credit scores. While providers claim most customers are creditworthy — Afterpay says it “over-indexes” in middle- and upper-income brackets — there are signs of strain:

- Klarna reported a 17% increase in credit losses year-over-year in Q1 2025, citing a surge in loan volume.

- LendingTree found 41% of BNPL users paid late in the past year, up from 34% in 2024.

- Affirm says defaults have fallen thanks to underwriting each transaction at the point of sale.

- Afterpay automatically freezes accounts after a single missed payment.

Regulation — and the Credit Reporting Debate

In 2024, the CFPB issued a rule to apply credit card regulations to BNPL providers. However, after political shifts in Washington, the agency announced it would not prioritize enforcing that rule.

Meanwhile, credit scoring is adapting:

- In June 2025, FICO announced it will include BNPL loans in credit reports.

- Affirm already shares repayment data with TransUnion.

- Klarna and Afterpay have held back, citing concerns about customers being penalized under outdated scoring models.

Both companies say they support frameworks that allow BNPL use to positively impact credit scores, but they want a dedicated scoring system rather than forcing BNPL into credit card metrics.

BNPL vs. Credit Cards: Replacement or Complement?

BNPL providers often present themselves as disruptors, aiming to replace high-interest revolving credit.

- Afterpay’s leadership has said “nothing would make our team happier than the death of revolving credit in the U.S.”

- Industry analysts believe BNPL will replace credit cards for certain transactions or certain groups, but not entirely.

Risks for the Future

As BNPL expands into new categories and demographics, providers face three major challenges:

- Rising Credit Losses — Expansion often means serving riskier customers.

- Regulatory Uncertainty — Shifts in political priorities could change compliance costs overnight.

- Macroeconomic Pressures — If consumer spending slows, BNPL defaults could rise sharply.

Despite these risks, the sector’s growth trajectory shows no sign of slowing — particularly with major players investing in physical retail partnerships and alternative credit scoring.

FAQs: Buy Now, Pay Later Explained

1. How does BNPL differ from credit cards?

BNPL offers fixed, short-term installment plans (often four payments) without interest, while credit cards allow revolving debt with variable interest rates. Merchants, not consumers, pay most BNPL fees.

2. Is BNPL good for your credit score?

It depends. Affirm reports some loans to credit bureaus, while Klarna and Afterpay currently do not. Starting in 2025, FICO will include BNPL in credit scoring, but how it impacts scores will vary.